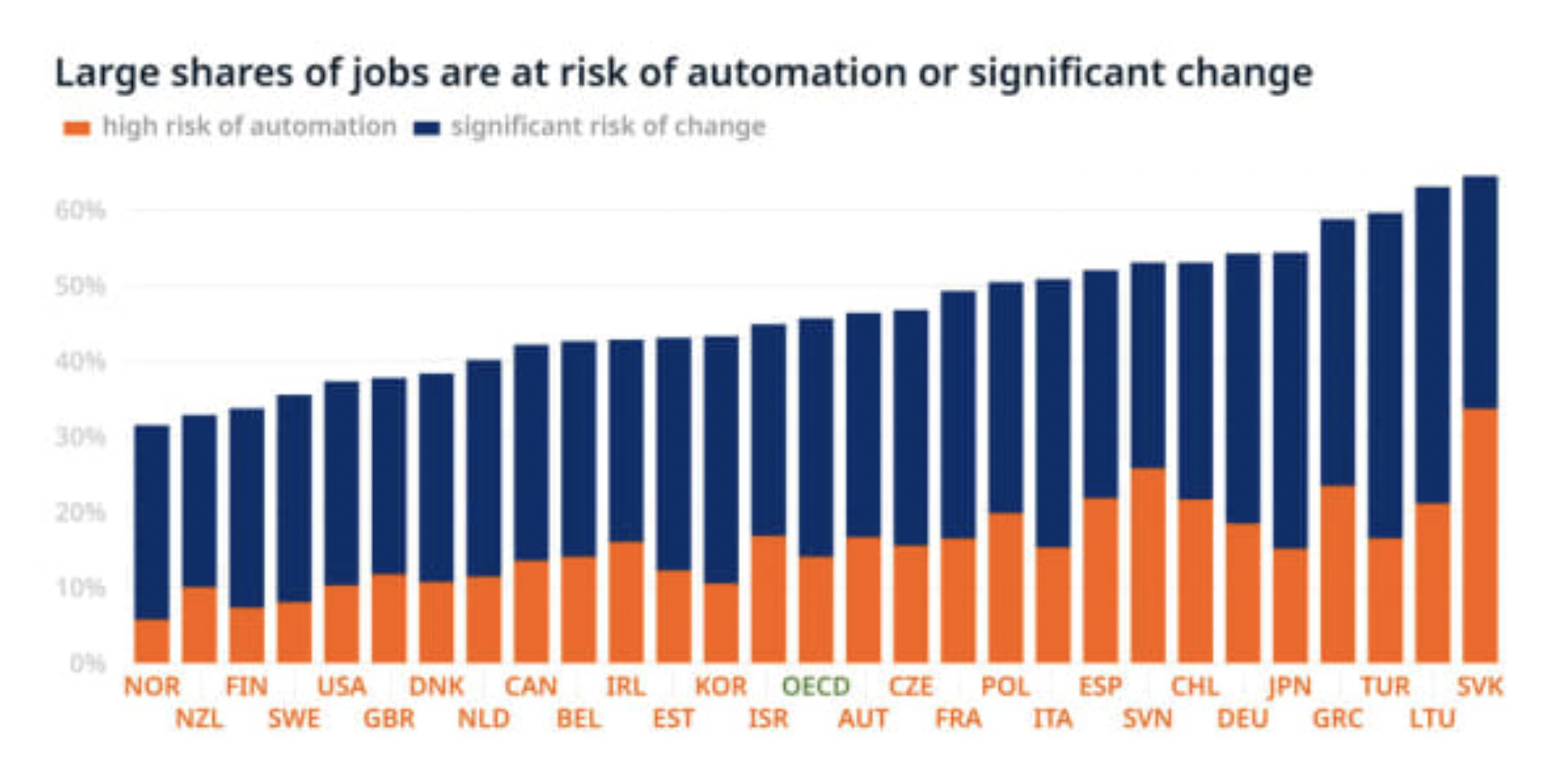

Thank you to those who attended the webinar that was recently concluded on 28 April 2022. For those who missed it, we hope this highlights article will give you good insights as to what was shared! The webinar was broken down into the following segments: We started off with this segment to give attendees the full context of what we mean by sales and process efficiency. This was done by taking the approach of looking back in time and then comparing it to the times we are in right now. The following chart form a report byOrganisation for Economic Co-operation and Development (OECD) was shown: It was shared that technology drives efficiency and eases workload. But it also potentially replaces the jobs of many. Almost half of all jobs could be wiped out or radically altered in the next two decades due to automation. However, the speaker also shared that specifically for intermediaries in the insurance industry, that if intermediaries constantly search for ways to be on the right side of technology – harness the power rather than be overpowered, this trend will not be something that will impact them. It was also shared that here in Singapore, we see the government already trying to act ahead of the curve to encourage digital transformation; for example, the Digital Acceleration Grant for insurance intermediaries announced by MAS at the middle of this year. To further prove this point, the following quote by John Maynard Keynes from the year 1930 (British economist, whose ideas fundamentally changed the theory and practice of macroeconomics and the economic policies of governments) was shared with attendees:

We are being afflicted with a new disease of which some readers may not yet have heard the name, but of which they will hear a great deal in the years to come–namely, technological unemployment. This means unemployment due to our discovery of means of economising the use of labour outrunning the pace at which we can find new uses for labour. But this is only a temporary phase of maladjustment. All this means in the long run that mankind is solving its economic problem.

Essentially, there was a huge lost of jobs as technology started picking up – however, as John Maynard Keynes rightly predicted (now with hindsight), it is only a period of maladjustment and in the long run, we have invented tech to solve or handle our economic problems by being more productive. The key takeaway, looking at this, is that intermediaries should look to harness the power of technology rather than be overpowered by it. This thought on the importance of the role of the intermediary as a human advisor was further echoed in an interview article with the president of GIA in April. The following excerpt was shared:

But while we are observing a growing preference for purchasing general insurance products digitally, our survey work with YouGov also reaffirmed consumers’ preference for the human touch – purchasing policies from agents and brokers – even among digital natives. Despite operating remotely, general insurance representatives play a critical role in enabling the sector to fulfil its promise of protecting customers, boosting financial literacy, and narrowing protection gaps. To this end, efforts to expand the talent pool and upskill the sector workforce to keep pace with an increasing digital economy should and will continue to be a priority for the sector.

We then switched gear to focus on the times we live in right now, amidst the pandemic and how we have learnt to adopt tech for our own betterment (whether by choice or not). We have learnt the benefits of automation We have learnt to work more collaboratively with peers We have learnt to free up more time by leveraging tech We then jumped into decoding the specific pain points that we understand hinders intermediaries when it comes to sales and process efficiency. Tedious quote sourcing practices Manual, labour intensive tracking of deals Slow network growth We then shared that in a recent survey we had conducted, the top 3 pain points intermediaries faced today (ranked by % selected) were The first segment of the webinar concluded that many of the pain points are related to manual and laborious processes. Sales and process efficiency basically means not being hindered by such to scale your business. Attendees were then taken to the next segment of the webinar that touches on the idea of what can be expected when intermediaries leverage tech to drive efficiency. The first point shared was that this will result in Zero GI business leakage The leaky bucket Having defined what we mean by ‘leaky bucket’, we went on to breakdown what causes such. Cause of the leaky bucket: ‘too troublesome’ Technology can drive greater efficiency to enable intermediaries in similar situations to be able to work with insurers and peers via automation! Cause of the leaky bucket ‘too complicated’ Technology can provide automated guidance through templated forms, suggestions and process ‘hand-holding’ Cause of the leaky bucket ‘small money’ Technology makes light work of previously tedious tasks, so that this supposed ‘small money’ is income that you can easily keep. Sharing about the ‘leaky bucket’ and the reasons for such is to heighten the awareness amongst attendees that tech helps to minimise hassle to allow you to capitalise on business opportunities! We then shared about yet another benefit that can be derived from a highly efficient process; that of a supercharged relationship between intermediaries and insurers. There are enough evidence in the industry today that showcases the fact that this is as important an initiative for the intermediary as much as it is for the insurer. Supercharging the efficiency of the sales force Research online, purchased offline Research has shown that the majority of customers still WANT to hear from a physical salesperson, even at the early stages of their research. What has changed is the expectations of the customer, when they speak to an intermediary. Syncing the two worlds Tech will remove efficiency barriers but one needs to be mindful to not ‘over-digitise’ and for insurers to run the risk of becoming ‘less human’. Of course, the goodness of tech is what we propound. However, it was also shared that intermediaries should do so for the right reasons! The speaker started this segment by using the analogy of ‘adding chill to laksa’ and said You add chilli to your laksa to make it spicier. And you do it because you like it spicier.

Not because you see everyone adding chilli and you just follow suit right?

Essentially, trying to drive home the point that one should not just follow a trend just because it is a trend! Do it because it helps the business. WHY Expand your network digitally to get more referrals The above table was shared to illustrate identifying the ‘why’ and then determining the ‘how’. Going back to the Laksa analogy… the ‘WHY’ = I want my laksa to be spicier. the ‘HOW’ = add chilli! Essentially, tech is available to help rid process and sales efficiency barriers. But how you leverage it and how the users are trained to use it will require effort. We entered the last segment of the webinar by sharing how, whether we like it or not, that the digital evolution has begun. What this digital evolution entails is that expectations of the customers have vastly changed as well – they know how technology IS available and will expect a more efficient experience. Having said that, the new age intermediary will still have their place in the ecosystem and an important one as long as they focus more on consulting instead of selling. To uplay their advisory skills now that they can leverage technology to free more time to do so. We took the opportunity to also share about the new and improved version of Surer and showcased its many features including Check out this demo video for an idea of how the above features work to solve your biggest pain points: We also shared with attendees that they can sign up for this new version of Surer for FREE and would love to extend this offer to that who are reading this article because you couldn’t make it for the webinar! Thank you to those who took time out to join us at the webinar. We hope it was a fruitful session for you. For those who are reading our highlights because you couldn’t make it, we hope this article gave you a good summary of the content shared! Subscribe to our Telegram channel or stay tuned to our Facebook or LinkedIn pages to get updates on more of such initiatives! It is fuss-free. No credit card or payment required.Key highlights

What does sales and process efficiency really mean?

How the pandemic has ‘forced’ this upon us

Decoding sales and process efficiency related pain points of an intermediary

In a highly efficient world, what are the tangible benefits for your business

Zero GI business leakage

‘Wah this client ask so many things, want so many quotes. I only have one GI principal… too leceh. Forget it lah.’

‘‘Too complicated lah. This GI is not my area of expertise. Forget it lah.’’

‘‘This deal, how much only. Not worth the work. Forget it lah.’’

Supercharged relationship and processes with insurers

Digitalise for the right reasons

Know your why… then think about how

HOW

I want to close a deal faster

Cut out all the (repetitive) effort you have to put in to source for multiple quotes

I want ease in managing my business

Automate the tracking of all your deals (past, present or future)

I want to close more deals

The digital evolution has begun

Unveiling the new and improved version of Surer!

SIGN UP FOR FREE HERE

Are you an Insurance intermediary? Sign up for free now!

Subscribe to our Telegram channel to get the most insightful articles delivered to you automatically!